Two Stocks to Buy Now and Hold for Five or More Years

Tesla

Amid the ongoing shift towards green energy, Tesla stands out as an enticing long-term investment, provided investors are willing to overlook short-term concerns related to margin contraction. As the undisputed leader in the electric vehicle (EV) sector, Tesla is poised to capitalize on the growing adoption of EVs. This advantage stems from its relentless focus on innovation, a robust portfolio of high-performance fully electric vehicles, and an extensive global network of Superchargers. Furthermore, Tesla’s prowess in developing technologies and software for self-driving vehicles, including its proprietary Full Self-Driving (FSD) tech, bodes well for future growth. It’s worth noting that Tesla’s stock has more than doubled year-to-date, albeit some recent retracement following the release of the company’s latest earnings report, primarily due to margin-related concerns. To provide context, Tesla has shifted its strategy towards boosting production volumes amid macroeconomic uncertainties and a high-interest rate environment. This entails lowering its average selling prices to stimulate sales, which, in turn, exerts pressure on margins and the stock price.

However, this pullback in Tesla’s stock price presents a compelling opportunity for investors. Tesla leverages its industry-leading margins to reduce average selling prices, thereby accelerating sales and challenging its competitors. In the short term, Tesla is willing to sacrifice margins to increase its fleet size and monetize FSD technology and software, establishing recurring revenue streams and enhancing margins.

Looking ahead, Tesla’s focus on expanding production capacity, cost reduction, and introducing new products will bolster its growth trajectory. Moreover, the acceleration of artificial intelligence (AI), the expansion of Supercharging services, and the integration of FSD technology are poised to significantly contribute to its profitability. Additionally, Tesla is ramping up the production of energy storage products and enhancing solar roof installation capabilities and efficiency, further fueling its growth prospects.

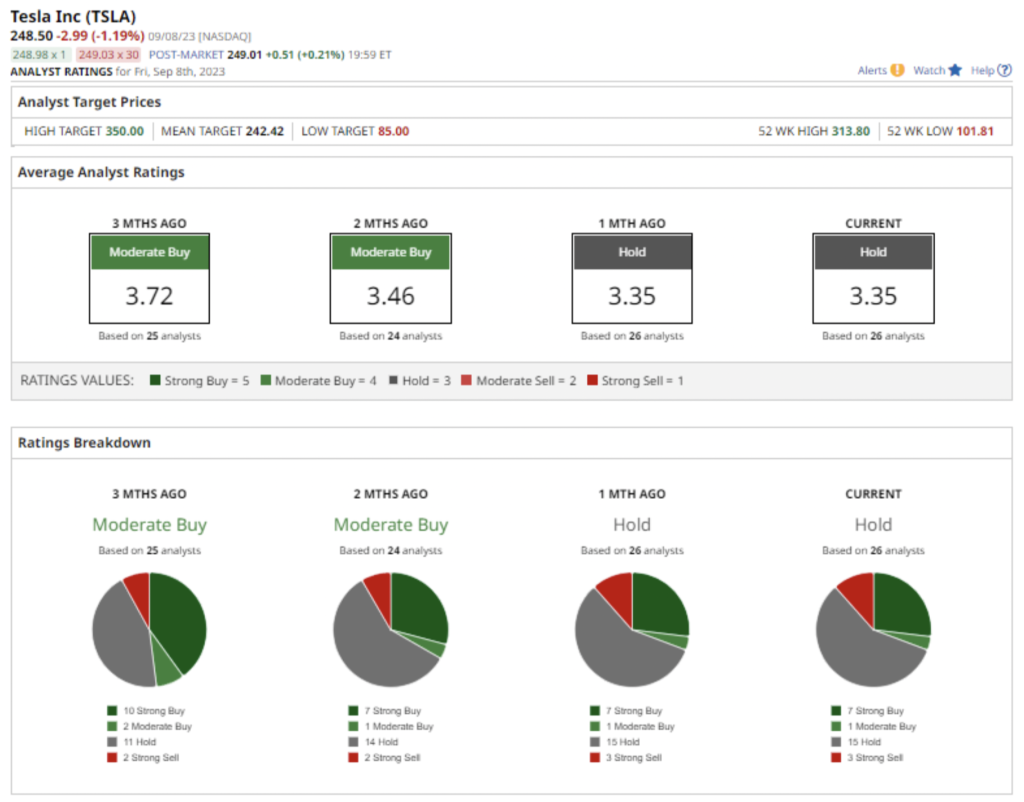

Nevertheless, it’s worth noting that, possibly due to the near-term margin pressures and the substantial year-to-date rally in the stock price, the majority of analysts maintain a cautious stance on Tesla. Out of 26 analysts covering TSLA stock, 15 rate it as “Hold,” three give it a “Strong Sell” rating, one recommends a “Moderate Buy,” and seven analysts suggest a “Strong Buy.” Their 12-month average price target for Tesla is approximately $242.42, representing a modest 8% downside from its current market price.

To provide context, Tesla has shifted its strategy towards boosting production volumes amid macroeconomic uncertainties and a high-interest rate environment. This entails lowering its average selling prices to stimulate sales, which, in turn, exerts pressure on margins and the stock price.

However, this pullback in Tesla’s stock price presents a compelling opportunity for investors. Tesla leverages its industry-leading margins to reduce average selling prices, thereby accelerating sales and challenging its competitors. In the short term, Tesla is willing to sacrifice margins to increase its fleet size and monetize FSD technology and software, establishing recurring revenue streams and enhancing margins.

Looking ahead, Tesla’s focus on expanding production capacity, cost reduction, and introducing new products will bolster its growth trajectory. Moreover, the acceleration of artificial intelligence (AI), the expansion of Supercharging services, and the integration of FSD technology are poised to significantly contribute to its profitability. Additionally, Tesla is ramping up the production of energy storage products and enhancing solar roof installation capabilities and efficiency, further fueling its growth prospects.

Nevertheless, it’s worth noting that, possibly due to the near-term margin pressures and the substantial year-to-date rally in the stock price, the majority of analysts maintain a cautious stance on Tesla. Out of 26 analysts covering TSLA stock, 15 rate it as “Hold,” three give it a “Strong Sell” rating, one recommends a “Moderate Buy,” and seven analysts suggest a “Strong Buy.” Their 12-month average price target for Tesla is approximately $242.42, representing a modest 8% downside from its current market price.

That being said, TSLA has recently seen an uptick in trading, driven by a bullish endorsement from Morgan Stanley, which assigned the stock a new Street-high price target and upgraded it to the equivalent of a “Strong Buy.” The analyst, Adam Jonas, set a price target of $400, citing optimism surrounding Tesla’s AI-driven “Project Dojo.”

Amazon

With its dominant presence in e-commerce, cloud services, and a burgeoning advertising division, Amazon is well-positioned to deliver robust returns over the long term.

Amazon’s stock has already surged by over 64% year-to-date. However, its relentless focus on cost reduction and profitability enhancement establishes a solid foundation for future growth.

That being said, TSLA has recently seen an uptick in trading, driven by a bullish endorsement from Morgan Stanley, which assigned the stock a new Street-high price target and upgraded it to the equivalent of a “Strong Buy.” The analyst, Adam Jonas, set a price target of $400, citing optimism surrounding Tesla’s AI-driven “Project Dojo.”

Amazon

With its dominant presence in e-commerce, cloud services, and a burgeoning advertising division, Amazon is well-positioned to deliver robust returns over the long term.

Amazon’s stock has already surged by over 64% year-to-date. However, its relentless focus on cost reduction and profitability enhancement establishes a solid foundation for future growth.

Amazon’s cost-cutting initiatives enable it to invest in improving delivery speed and expanding its range of everyday essentials, driving increased website traffic and larger order sizes.

Earlier this year, Amazon Web Services (AWS), the cloud-based division of Amazon, faced headwinds due to macroeconomic factors. Nevertheless, AWS has successfully maintained its leadership in the cloud infrastructure sector. During the Q2 conference call, Amazon’s management indicated signs of stabilization in the business, a positive development. Furthermore, the reacceleration of growth in AWS, coupled with the integration of generative AI capabilities into its platform, bodes well for future expansion.

Alongside AWS, Amazon is poised to benefit from the sustained momentum in its advertising business. Despite macroeconomic uncertainties, Amazon’s advertising revenue has witnessed consistent growth, with a 20% increase reported over the past six consecutive quarters. Moreover, the company leverages machine learning and performance-based advertising to provide added value to its customers, further supporting future expansion.

In summary, Amazon’s expanding Prime membership, robust digital advertising presence, resurgent growth in AWS, and integration of AI into its services lay a robust foundation for sustained long-term growth.

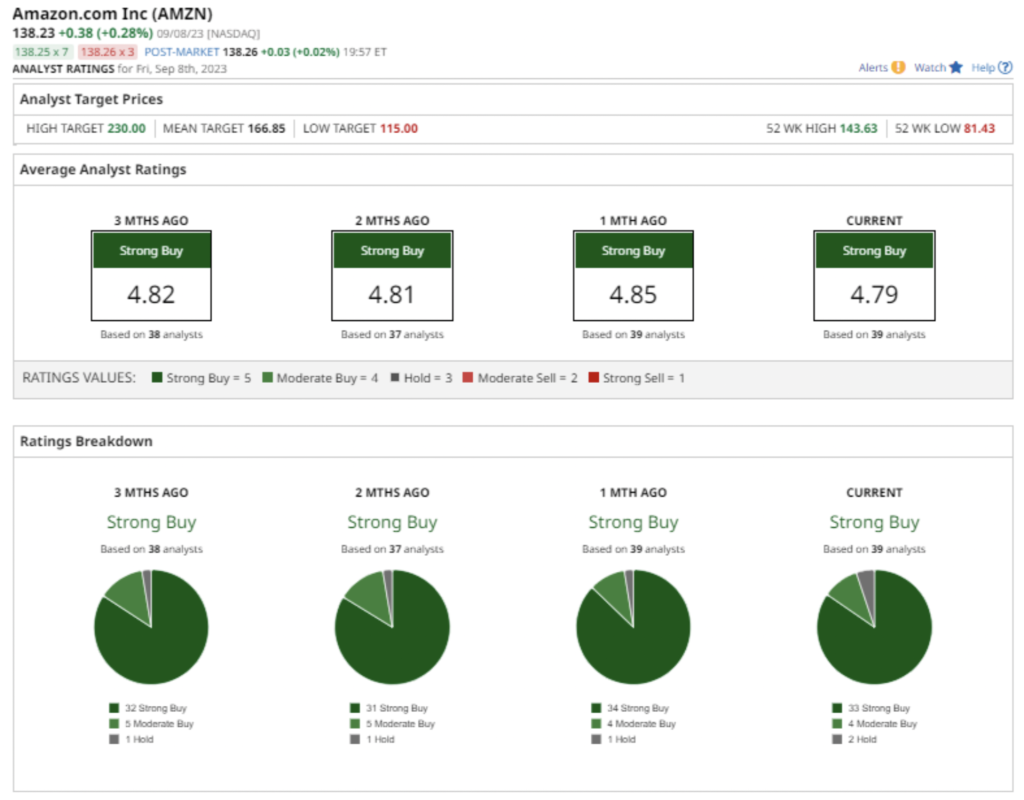

Encouragingly, the improving operating trends have garnered favorable opinions from most analysts covering AMZN stock. Out of 39 analysts providing coverage, 33 recommend a “Strong Buy” rating, four suggest a “Moderate Buy,” and two maintain a “Hold” rating. Additionally, the average price target for Amazon stands at $166.85, implying an anticipated upside of over 18% from its current valuation.

Amazon’s cost-cutting initiatives enable it to invest in improving delivery speed and expanding its range of everyday essentials, driving increased website traffic and larger order sizes.

Earlier this year, Amazon Web Services (AWS), the cloud-based division of Amazon, faced headwinds due to macroeconomic factors. Nevertheless, AWS has successfully maintained its leadership in the cloud infrastructure sector. During the Q2 conference call, Amazon’s management indicated signs of stabilization in the business, a positive development. Furthermore, the reacceleration of growth in AWS, coupled with the integration of generative AI capabilities into its platform, bodes well for future expansion.

Alongside AWS, Amazon is poised to benefit from the sustained momentum in its advertising business. Despite macroeconomic uncertainties, Amazon’s advertising revenue has witnessed consistent growth, with a 20% increase reported over the past six consecutive quarters. Moreover, the company leverages machine learning and performance-based advertising to provide added value to its customers, further supporting future expansion.

In summary, Amazon’s expanding Prime membership, robust digital advertising presence, resurgent growth in AWS, and integration of AI into its services lay a robust foundation for sustained long-term growth.

Encouragingly, the improving operating trends have garnered favorable opinions from most analysts covering AMZN stock. Out of 39 analysts providing coverage, 33 recommend a “Strong Buy” rating, four suggest a “Moderate Buy,” and two maintain a “Hold” rating. Additionally, the average price target for Amazon stands at $166.85, implying an anticipated upside of over 18% from its current valuation.

Get back to Seikom News 🤓

Latest Posts

December 10, 2024

December 10, 2024

Is the AUD Oversold Ahead of the RBA Decision?

As the Reserve Bank of Australia (RBA) prepares for its final meeting of the year, inflation remains a significant hurdle to cutting interest rates. Analysts predict that any adjustments will likely occur in 2024, with projections ranging from February (Commonwealth Bank) to the June quarter (NAB). This week, the RBA will convene to deliberate on […]

Read more December 5, 2024

December 5, 2024

Global Currencies Stage a Comeback Amid Political and Market Shifts

Global Currencies Stage a Comeback Amid Political and Market Shifts The week began with robust demand for the dollar, fueled by President-elect Trump’s pointed warnings to BRICS nations about adopting a currency alternative to the US dollar. Adding to the volatility, political unrest in France has raised concerns about a potential government collapse. However, […]

Read more November 30, 2024

November 30, 2024

Dollar Slips as Thin Trading Conditions Dominate Pre-Holiday Markets

Wednesday’s U.S. data releases, largely aligning with expectations, shifted market focus to month-end flows, which worked against the dollar. A wave of broad dollar selling coincided with a dip in risk appetite, evident in the weaker performance of U.S. equities. Looking ahead, Thursday’s key events include German inflation figures and Eurozone sentiment data. However, with […]

Read more November 25, 2024

November 25, 2024

Crypto vs. Gold: The Ongoing Battle for Investor Focus

November 25, 2024 Despite the allure of cryptocurrencies, gold remains a strong contender, marking its best weekly performance in nearly two years and trading just 3% below its October 30 peak. State Street Global Advisors has expressed concerns about the current cryptocurrency rally overshadowing gold. Nevertheless, gold continues to climb, with XAU/USD maintaining an upward […]

Read more